Insurance companies vary greatly from one another. These differences span the certain products they sell, the specific geographies they operate in, and the different points in the value chain where they sit. However, when you strip away these differences, insurance companies require the same fundamental software, which can be put into three buckets:

- agency or policy management systems

- accounting software

- marketing platforms

Besides these core systems, myriad enhancements can be ‘plugged in or bolted on’ to increase functionality. Another key criterion for these essential systems is the level of extensibility within and outside of their ecosystem. According to Techopedia, extensibility is a measurement of a piece of technology's capacity to append additional elements and features to its existing structure. A software program, for example, is extensible when its operations may be augmented with add-ons and plugins. For example, does a single vendor provide all three of these core systems, or is a company left to find three separate systems that it can make work together?

It's practically impossible to provide a comprehensive list of all existing software vendors in the market. Moreover, new and innovative software is constantly being introduced in the insurance industry, which can alter how core systems are perceived and whether a 'one and done' or 'best system for the job' approach is more suitable. As a solution, we'll delve into the primary criteria that serve as the foundation for these core systems, which are widely applicable throughout the insurance sector.

How Insurance Works

Before we can begin to describe the commonalities between core insurance systems, we must first make sure that you understand the internal workings of the industry. At every point in the insurance sales and policy administrative process, what you can describe as the value chain, unique needs emerge.

At the highest level, insurance exists to reimburse you for damage to your property or to pay others on your behalf when you injure someone or damage their property. Insurance (also described as risk transfer) is a contract that transfers the risk of financial loss from an individual or business to an insurance company. To pay for losses, these insurance organizations collect small amounts of money from clients and pool that money together to pay claims.

We divide insurance into two major categories:

- Property and Casualty insurance (P&C)

- Life and Health insurance

Property and casualty insurance protects individuals and companies for losses related to their belongings or assets, both physical and financial. Life and health insurance protect people from financial loss due to premature death, sickness, or disease.

Insurance uses probability and the law of large numbers (think actuarial science) to determine the cost of insurance premiums based on various risk factors such as past claims, region of the world, and information about you that is provided during the quoting process. The rate you pay must be sufficient for the insurer to pay claims in the future, its expenses, and retain a profit margin. The likelihood of a catastrophic event for a given client directly correlates to how much the policyholder will pay to the insurance company.

Insurers distribute their products and services in different ways. Some of the most common distribution models include direct to consumer (D2C), through an independent broker or agent, or embedded in another product. Each method of marketing and selling a product can require different software to support the distribution. The price companies charge for insurance coverage is subject to government regulation. Insurance companies may not discriminate against applicants or insureds based on a factor that does not directly relate to the chance of a loss occurring.

How Insurance Companies Operate

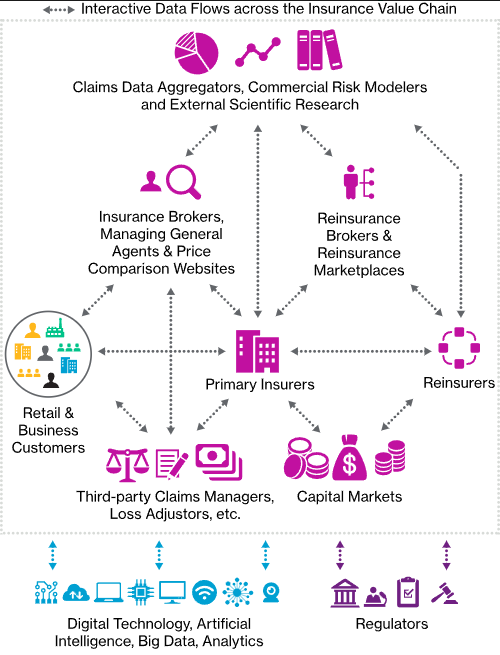

Now that we understand how insurance generally works, let’s dive into how an insurance carrier will operate. Agents, Brokers, Managing General Agencies (MGAs,) and wholesalers may have some of these five functions, but not all. This diagram from Willis Towers Watson shows the interactions between different insurance players.

Insurance companies are generally organized into five broad departments: claims, finance, legal, marketing, and underwriting. A good way to think of these departments is as a series of checks and balances to limit the insurer from taking on too much risk. Marketing and underwriting are the “yes” departments, while claims and finance are the “no” departments. The legal department is often the referee between the desire to sell more policies (and increase revenue) and limit claims (e.g., risk).

It is the underwriting department's job to develop insurance products that can be sold to their customers for a profit. While many application forms are standardized, some underwriting departments will craft their collection of specific information to gather during the application so that the marketing department can ‘say yes’ to as many individuals as possible.

The claims department reimburses the policyholder for damages to the insured assets, while the underwriting department rarely affects a decision to pay a claim. The marketing and underwriting departments are judged by their premium collections and retention ratios (i.e., the percentage of insureds who renew their policies with that insurer), while the claims department is judged by how little it incurs resolving claims. Thus, there is an inherent and perpetual tension among these departments. These financial measures drive insurance company management and profits, as well as the bonuses paid to department management.

Software that Most Insurance Companies Use

With a strong background on how the insurance industry and insurance companies operate, we can break down the systems that insurance companies use. Selling insurance starts with marketing. To that end, most insurance companies will use marketing software to create brand awareness among prospects. These same systems often will also allow insurance companies to bring up-sell and cross-sell opportunities (what is also called account rounding) to the attention of existing policyholders. Another feature that can be valuable in a marketing system is the capability to approach those nearing their renewal date with retention messaging and for those that have left, remarket products and services to them to regain their business.

Once the policy has been sold, the policy and policyholder information needs to be recorded somewhere. For this task, insurance companies will use an agency management system (AMS) or policy management system (PMS). This is important because of legal requirements to have a record of the in-force policies (currently legally binding).

Many AMS/PMS software is like very insurance-specific customer relationship (CRM) systems. However, there are plenty of examples of insurance companies using an AMS/PMS in conjunction with a CRM. Why might they do that? Some companies only want policyholders in their AMS and use CRM for marketing. There is no one right way for insurance companies to use software, however, the more systems that are used, the higher the potential is for duplicate records, manual keying errors, and out-of-date information. An AMS/PMS is the beating heart of any insurance company. It functions as the single source of truth in insurance, and without it, insurance companies have a difficult time operating.

Many AMS/PMS software bundle in other core functions like marketing. Other functions that are common to find bundled in, or used separately, include accounting, claims, and a rating system. Insurance companies must understand what their requirements are and will be in the future so that they can purchase the best system or set of systems to meet their needs.

In the age of insurtech, many emerging companies provide solutions to solve part or all of the insurance marketing, sales, administration, claims, and retention cycles. Insurtechs often provide functionality that legacy systems providers do not or frankly, cannot. As an example, some insurtechs are using artificial intelligence to boost retention and lower churn by identifying those that are most likely to leave as much as 6 months before the renewal date. To take advantage of these companies requires an innovative mindset and the ability to either get data out of a core system or connect software.

The Best Software for Insurance Companies

There are many different vendors of software for insurance companies. So the ‘best’ software for an insurance company will be business-specific, based on what the end-user needs it to do. Other important factors in selecting the best software include price, scalability, cloud-deployed or running on servers locally, and customization options, either through application programming interfaces (APIs) or a partner store.

Regardless of what the best software may be for a specific insurance company, all will use the same types of core systems to run their business and serve their customers. In many situations, it is far more affordable in the long term to buy rather than build these core systems. When any software is built in-house, it will cost approximately 10% per year of the original build cost to maintain it. In what can quickly become tens of millions of dollars in software development, buying is normally more scalable. Plus, when you buy software, you get the resources and support you need to customize and use it.